2000년 당시 IT 버블과 같은 패턴

Unjustly, some readers have called me a desperate crash prophet during the last few months.부당하게, 몇몇 독자들은 지난 몇 달 동안 나를 절망적인 충돌 예언자라고 불렀다. However, I have never presumed to time the stock markets. 그러나 나는 주식시장의 시기를 추정해 본 적이 없다. From my perspective, stocks are the best option for long-term wealth management, which is why I continue to invest capital every month. 내 관점에서는 주식은 장기적 재산관리에 가장 좋은 선택사항이고, 그래서 나는 매달 자본을 계속 투자한다. Therefore, I never endorsed a short position, trading, or anything similar. 그러므로 나는 단직이나 거래, 또는 이와 비슷한 것을 지지한 적이 없다. The central focus of my reflections was always the dichotomy that investors are currently facing. 내 성찰의 중심은 항상 투자자들이 현재 직면하고 있는 이분법이었다.On the one hand, we see historically high valuations, which are marginalized by a lack of alternatives on the other.한편으로, 우리는 역사적으로 높은 평가를 보는데, 다른 한편으로는 대안의 부족으로 인해 소외되고 있다. At the same time, central banks continue to pump new liquidity into the markets. 동시에 중앙은행들은 시장에 새로운 유동성을 계속 공급하고 있다. Even in a pure thought experiment, this constellation brings all the ingredients for a drama. 순수한 사고 실험에서도 이 별자리는 드라마의 모든 재료를 가져온다.If we follow the very similar development of the dot com bubble so far, we currently might see the beginning of the last phase before the burst, the hyperventilating speculation.지금까지의 닷컴 버블의 매우 유사한 발전을 따른다면, 현재 우리는 폭발 전에 마지막 단계의 시작인 과호흡 추측을 볼 수 있을 것이다. These patterns do not give us any certainty as to when which development will begin. 이러한 패턴은 우리에게 언제 개발이 시작될지에 대한 확신을 주지 못한다. However, it is high time for investors to review their investment approach and risk allocation. 다만 투자자들의 투자 방식과 리스크 배분을 검토할 때가 됐다. Here, too, the patterns of the dot com bubble help us. 여기도 닷컴 거품의 패턴이 우리에게 도움이 된다.Following the 2000 bubble pattern2000년 버블 패턴 이후

It is quite interesting how the current phase resembles the final phase of the dot com bubble.현재의 국면이 닷컴 버블의 최종 국면과 어떻게 닮았는지는 꽤 흥미롭다. In 2000, we also saw how the share price broke out of a multi-year upward trend, and if we look at the NASDAQ today, this same situation has already occurred. 2000년에도 다년간 상승세로 주가가 어떻게 빠져나갔는지 봤고, 오늘 나스닥을 보면 이미 이런 상황이 벌어진 것이다.

NASDAQ, dot com bubble, and current developments 나스닥, 닷컴 버블 및 현재 개발

We are not quite there yet with the S&P 500.우리는 S&P 500에 아직 도착하지 않았다. However, given the current sentiment, it should only be a matter of time before the S&P 500 breaks the long-term trend upwards to the north. 그러나 현재의 정서를 감안할 때 S&P 500이 장기적 추세를 북으로 꺾는 것은 시간문제일 뿐이다.

S&P 500, dot com bubble, and current developmentsS&P 500, 닷컴 버블, 현재 개발

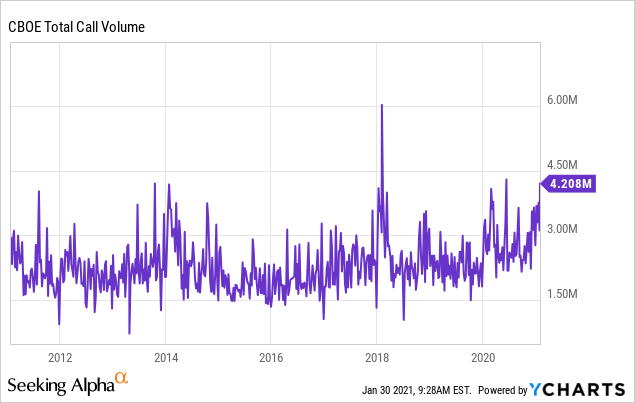

Both the NASDAQ and the S&P 500 continued to rise for quite some time in the dot com bubble after they had crossed the long-term trend.나스닥과 S&P 500지수도 모두 장기 추세를 넘은 뒤 닷컴 버블 속에서 상당 기간 상승세를 이어갔다. The interesting thing is that we have the same narratives and distortions both in the late stages of the dot com bubble and now. 흥미로운 것은 우리는 닷컴 버블의 말기와 현재 모두 같은 서술과 왜곡을 가지고 있다는 것이다. We see a shift in the motivation why people go with their capital in the stock market. 우리는 사람들이 주식시장에서 자기 자본을 가지고 가는 동기가 바뀌는 것을 본다. In the final phase of the bubble in 2000, as well as now, investors only bet on higher share prices without paying a single bit of attention to fundamental valuations: 2000년 버블의 마지막 단계인 현재와 마찬가지로 투자자들은 근본적인 가치평가에 전혀 신경 쓰지 않고 높은 주가에만 베팅하고 있다.For me, who wants to become an owner of companies and therefore wants to get a substance for his money and not just a coupon that might increase in value, this consideration was new. 기업의기업의 주인이 되고 싶어 가치가 상승할 수 있는 쿠폰이 아닌 자신의 돈으로 실물을 얻으려는 나에게 이런 배려가 새삼스러웠다. In this respect, the perspective has changed. 이런 점에서 관점이 달라졌다. A share is no longer the proof of ownership of a company but a kind of betting slip with which one can bet that share prices will rise. 주식은 더 이상 회사의 소유권 증명이 아니라 주가가 오를 것이라는 데 베팅할 수 있는 일종의 베팅 전표가 된다. With this change in perspective, the focus has shifted significantly from investing to speculating. 이런 관점이 바뀌면서 투자에서 투기로 초점이 크게 바뀌었다.Besides, we see a high level of speculation.게다가, 우리는 높은 수준의 투기를 본다. The number of option contracts is increasing. 옵션 계약 건수가 증가하고 있다.

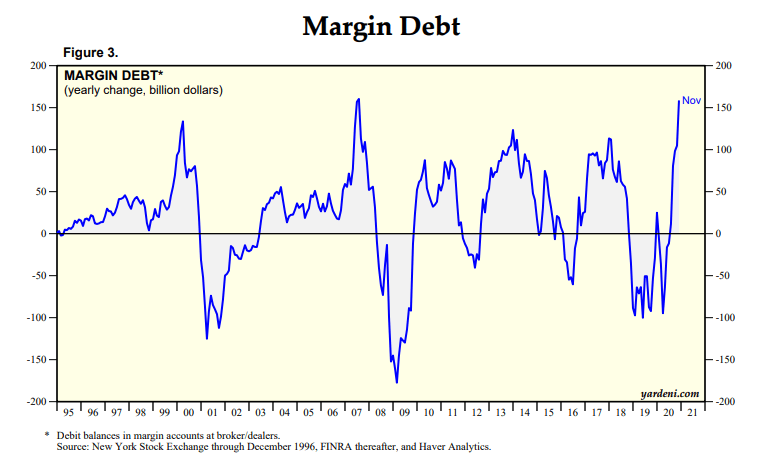

The speculation level is also associated with high margin debt, which causes an additional problem because with the amount of margin debt, the risk of a margin call increases.투기수준도 높은 마진부채와 연관돼 있어 마진부채 규모와 함께 마진콜 위험이 커지기 때문에 추가 문제가 발생한다.

The speculation level is also associated with high margin debt, which causes an additional problem because with the amount of margin debt, the risk of a margin call increases.투기수준도 높은 마진부채와 연관돼 있어 마진부채 규모와 함께 마진콜 위험이 커지기 때문에 추가 문제가 발생한다.

Source: Margin debt출처: 차액 채무

Other examples of parallels are easy to find.다른 유사 사례들은 찾기 쉽다. In addition to the number of IPOs of non-profitable companies and SPACs, the appearance of private retailers as a stock shifting and almost chaotic and anarchic force is precisely a circumstance that matches the expanding bubble in 2000. 비영리기업과 SPAC의 IPO 건수 외에도 민간 유통업체가 주식 시프트로 등장하고 거의 무질서하고 무정부적인 힘으로 등장한 것은 2000년 거품 확대에 정확히 필적하는 상황이다.Timing is not possible타이밍이 가능하지 않음

Despite all these parallels, it is impossible to time the next months, quarters, or even years.이 모든 유사점에도 불구하고, 다음 달, 분기, 심지어 몇 년의 시간을 맞추는 것은 불가능하다. Indeed, we see historically high valuations. 사실, 우리는 역사적으로 높은 가치를 본다. However, if we look at the Shiller CAPE ratio, there is even upside potential of over 30 percent until we reach the level of 2000. 하지만 실러 케이프 비율을 보면 2000년 수준에 도달할 때까지 30%가 넘는 상승 잠재력까지 있다. But what does that mean? 하지만 그것은 무엇을 뜻하나요? Nothing prevents shares from expanding their multiples even further. 어떤 것도 주식의 배수가 더 확장되는 것을 막을 수 없다.

Source: Board of Governors of the Federal Reserve System (US), fred.stlouisfed.org 출처: 연방준비제도 이사회(미국), fred.stlouisfed.org

Another worthwhile observation lies in comparing the historical P/E ratio of Treasuries with the Shiller CAPE ratio.또 다른 가치 있는 관찰은 채권의 과거 P/E 비율을 실러 케이프 비율과 비교하는 것이다. From this, you can see that stocks are pretty cheap compared to the 10-year treasury. 이를 통해 주식은 10년 만기 국고에 비해 상당히 저렴하다는 것을 알 수 있다.

Source: Reciprocal 10-year treasury bond yield vs. 출처:출처: 상호 10년 만기 국고채 수익률 vs. S&P 500 forward P/E S&P 500 포워드 P/E

We can also compare the current margin debt level with the total market cap.현재 마진 부채 수준과 시가총액을 비교할 수도 있다. Here, we can see that we are below the 2000 level and far below the period from 2006 to 2018. 여기서 우리는 2006년부터 2018년까지의 기간과 2000년 수준을 훨씬 밑돌고 있음을 알 수 있다.

Source: FINRA Margin Debt Relative to Total Market Cap출처: 총 시장 상한 대비 FINRA 마진 채무

Avoiding the pain고통을 피한다.

Investing, in my view, is not camp thinking but should always be free of any bias.내가 보기에 투자는 캠프의 사고가 아니라 항상 어떤 편견으로부터 벗어나야 한다. We have to admit that we don't know where things are headed in the medium term. 우리는 중기적으로 상황이 어디로 향하는지 모른다는 것을 인정해야 한다. Nevertheless, I think we can state the following. 그럼에도 불구하고, 나는 우리가 다음과 같이 말할 수 있다고 생각한다. A continuation of the current rally, especially in the tech sector, depends on certain conditions: 특히 기술 부문의 랠리를 계속하려면 다음과 같은 특정 조건에 따라 달라진다.- Money supply/liquidity,통화 공급/유동성,

- lacking alternatives (bonds etc.),대안 부족(대안 등),

- lacking inflation.인플레이션이 없는

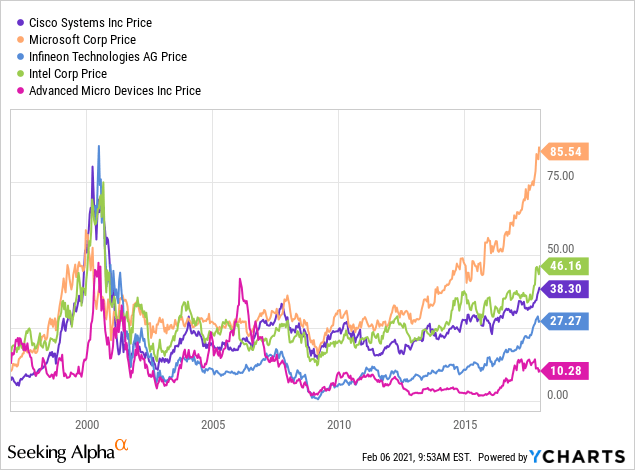

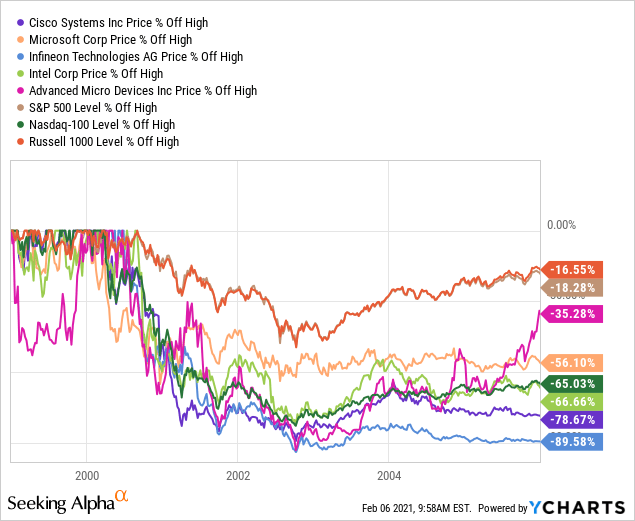

one move of a legislator's pen can turn entire libraries into wastepaper. 국회의원의국회의원의 펜 한 번으로 도서관 전체가 휴지 조각이 될 수 있다.So if "keep up the bull market" depends on uncertain narratives rather than fundamentals, I think the best thing to do is to focus on the first rule of investing: "Don't lose money."그래서 펀더멘털보다는 불확실한 내러티브에 의존하는 '황소시장 유지'가 가장 우선시되는 것이 투자 첫 번째 룰인 '돈 잃지 마라'에 집중하는 것이라고 생각한다. So for me, it's about taking a risk-reducing approach in the current market phase. 그래서 나에게 있어, 그것은 현재의 시장 단계에서 위험을 줄이는 접근법을 취하는 것이다. In this way, I want to avoid the significant pain that could otherwise occur in a worst-case scenario. 이런 식으로 나는 최악의 시나리오에서 일어날 수 있는 중대한 고통을 피하고 싶다. Here, too, we can use the parallels from 2000. 여기에서도 2000년부터 유사점을 사용할 수 있다. For me, it's about protecting my assets. 나에겐 자산 보호에 관한 겁니다. In the graph below, we see a selection of hyped stocks at the peak of the dot com bubble. 아래 그래프에서 우리는 닷컴 버블의 정점에 있는 과대 포장된 종목을 볼 수 있다. You can easily see that it makes a huge difference whether someone was invested in Microsoft (MSFT) in 1995 or started buying shares in 2000. 1995년 MSFT(마이크로소프트)에 투자됐든 2000년부터 주식을 사들이기 시작했든 큰 차이가 난다는 것을 쉽게 알 수 있다. The same is true for Cisco (CSCO) and other stocks. 시스코(CSCO) 등 다른 종목도 마찬가지다.

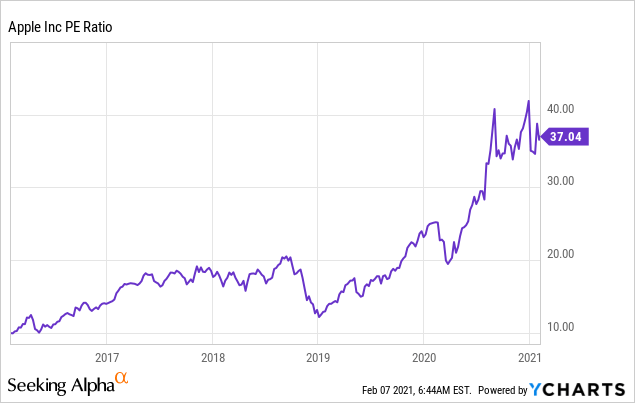

The picture of today's market is comparable.오늘날 시장의 모습은 비견할 만하다. Look at what a difference two years make at Apple (AAPL). 애플(AAPL)에서 2년의 차이가 얼마나 큰지 보라. The company was an incredible bargain in early 2019. 그 회사는 2019년 초에 믿을 수 없는 흥정이었다. I wouldn't even think of selling my Apple stock. 나는 애플 주식을 팔 생각도 하지 않을 것이다. If the price collapses like it did in 2000, so be it. 2000년처럼 가격이 무너지면 그렇게 될 것이다. In the worst case, I lose my book profits, slide into minus and then have the chance to repurchase Apple shares as a bargain. 최악의 경우 나는 장부상 이익을 잃고 마이너스로 빠져들다가 애플 주식을 헐값으로 되팔 기회를 갖게 된다. But if I buy now, I have enormous downside risk, and I don't want to wait 10 to 15 years until I slide back into positive territory, as was the case with Microsoft, for example. 하지만 지금 구매한다면 엄청난 하방 리스크를 안고 있으며, 예를 들어 마이크로소프트의 경우와 마찬가지로 긍정적인 영역으로 다시 미끄러질 때까지 10년에서 15년을 기다리고 싶지 않다.

What do I do with my capital instead?대신 내 자본을 어떻게 하지? I continue to invest in the equity market. 나는 주식 시장에 계속 투자한다. Still, given the fundamental valuation multiples, it is not the right time to bet on growth stocks with exploded multiples. 그러나 근본적인 밸류에이션 배수로 볼 때 지금은 폭발적으로 늘어난 배수로 성장주에 베팅할 때가 아니다. You can see what I want for my portfolio instead by comparing the high flyers of the dot com bubble with more broadly diversified indexes. 닷컴 버블의 높은 전단지들과 좀 더 다양한 인덱스를 비교해 보면 내가 포트폴리오를 위해 무엇을 원하는지 알 수 있다. So I believe that putting your money in conservative and somewhat rationally valued companies is the better approach right now when it comes to the first rule of investing. 그래서 나는 당신의 돈을 보수적이고 다소 합리적으로 가치가 있는 회사에 투자하는 것이 투자라는 첫 번째 규칙에 관한 한 지금 당장 더 나은 접근법이라고 믿는다.

Conclusion결론

So to wrap it up: I am convinced that as long as we pursue a rational approach that takes fundamental data into account and follows a long investment horizon, we have nothing to fear in the long-term.결론부터 말하자면, 나는 우리가 근본적인 데이터를 고려하고 긴 투자 지평을 따르는 이성적인 접근법을 추구하는 한, 장기적으로는 두려워할 것이 없다고 확신한다. I continue to invest stubbornly and steadily in stock markets. 나는 주식시장에 완강하고 꾸준한 투자를 계속하고 있다. However, current sentiment markets suggest that rational sentiment has increasingly given way to emotional mania, chaos, and greed. 그러나 현 감정시장은 이성적 정서가 갈수록 감정 마니아, 혼란, 탐욕에 밀려났음을 시사하고 있다. Therefore, keeping it simple with a risk-averse approach and not trying to follow every hype might be the best advice right now. 따라서 위험을 회피하는 접근법으로 단순하게 유지하고 모든 과대 광고를 따르지 않는 것이 지금 당장 가장 좋은 조언이 될 수 있다.Some companies named in this article are part of my diversified retirement portfolio. 이이 글에 이름이 붙여진 몇몇 회사들은 나의 다양한 은퇴 포트폴리오의 일부분이다. If you enjoyed this article and wish to receive other long-term investment proposals or updates on my latest portfolio 만약 당신이 이 기사를 즐기고 나의 최신 포트폴리오에 대한 다른 장기 투자 제안이나 업데이트를 받고 싶다면 research, click "Follow" next to my name at the top of this article, and check "Get email alerts". 이이 글의 맨 위에 있는 내 이름 옆에 있는 "팔로우"를 클릭하고 "전자 메일 알림 받기"를 선택하십시오.

댓글